What does the current cattle price mean for producers?

Both domestic and international factors will have positive and negative influences on Australian cattle prices over the coming 12 – 24 months. This month we will touch on the Australian domestic cattle supply situation.

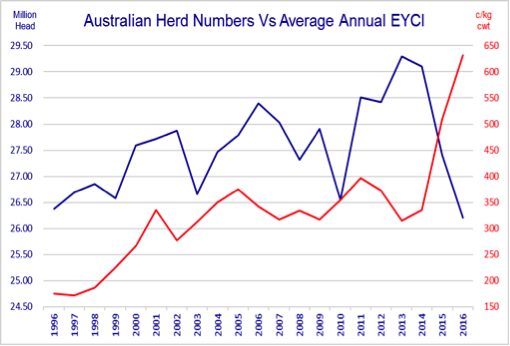

The Australian cattle herd is predicted to drop to 26.2 million head in 2016, its lowest level in 24 years. A combination of high cattle prices and extended drought conditions has led to an unprecedented selloff of adult and female cattle over the past three years which has resulted in the herd numbers dropping 12% since 2013.

The differential between livestock pricing and supply has not been as great since the EYCI first began recording in 1996 and highlights entry into a phase of extensive herd rebuilding, lower slaughter of female cattle and increased competition and pricing for a limited pool of slaughter cattle.

What does this mean for producers?

- Along with cattle prices, demand for feedlot and slaughter cattle will remain high over the next year, although not at their current peak. We feel that without considering possible market based interruptions, an average summer rainfall season over the northern part of the country, and continued competition between restockers; feedlots and processors will keep pricing within a range of 550c/kg to 590c/ckg cwt over the coming calendar year.

- Female cattle including cull cows; yearling heifers and PTIC females will be in strong demand as producers look to replace cattle sold during the drought. We feel that stock cattle pricing over the past two years has resulted in reduced financial pressure for producers to market 100% of their cull female cattle, and combined with excellent spring rainfall and an average summer season, producers are uniquely positioned to run increased numbers of female cattle over the breeding season.

- We believe that with average to strong seasonal conditions, the rebuilding of herd numbers will bounce back to average levels within 2-3 years. High prices and an excellent 2016 spring season are actively encouraging producers to hold females (rather than trade), and a lower proportion of females within total adult cattle slaughter also supports this view.

Let us know your view on LinkedIn